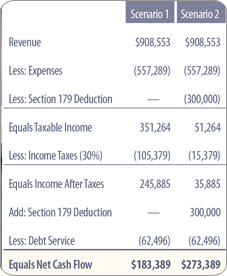

Scenario 1 is pretty simple and typical in nature. Scenario 2 generates $90,000 in tax savings for a simple reason: Section 179. The customer

purchased $300,000 of equipment that was placed into service during the tax year. At an assumed tax rate of 30%, the taxpayer gains a deduction

of $300,000, which results in additional take-home cash of $90,000.

Three golden rules

There are three rules of Section 179 you cannot forget. First, the deduction is allowed only in the year that the asset is “placed into service.”

This means the year in which the equipment is ready for use, not the year in which the equipment is purchased. Second, Section 179 applies to

personal property, such as equipment and technology, and potentially leasehold improvements. Third, the deduction is limited to $500,000 of

equipment purchases in a single year. Equipment that qualifies for the deduction but exceeds $500,000 can be depreciated across future tax years.

The deduction isn’t lost; it’s simply delayed.

ARTICLE TOOLS

PRINT

PRINT

SHARE

SHARE

Separate from Section 179 is the concept of bonus depreciation. Like Section 179, this is also a section of the tax code that has been subject to change

due to politics. Bonus depreciation is a deduction that is allowed on equipment that has not been recognized under Section 179. How much can be

deducted? Fifty percent of the cost to acquire. Let’s clarify with our final example.

Assume for a moment you’re purchasing equipment for a remodel. Five operatories of equipment, a sterilization center, a CEREC, and a Galileos

cone beam, totaling $720,000. Also assume an effective tax rate of 30%. The first $500,000 of the total cost would be subject to Section 179

deduction and would create a tax savings of $150,000 ($500,000 x 30%). The remaining $220,000 would be subject to the 50% bonus depreciation and

would create a tax savings of $33,000 (($220,000 x 50%) x 30%). The total first-year tax savings on a $720,000 investment in a renovation: $183,000!

Taking the leap

So how do you decide whether this is the year to take advantage of Section 179? First, understand this principle of finance: Do not invest in an

asset solely for the purpose of saving taxes. Spending money for this single purpose means that you spend a greater amount of money than the tax

savings.

Second, accept this principle of finance: Invest in assets that will generate a positive rate of return. Purchasing assets such as a CEREC that

can generate future income in excess of the cost to acquire the machine is a drastically different investment than “investing in a boat,” which

will not have a return on investment.

Last, and most importantly, ponder whether the equipment or technology you’re looking at truly improves or maintains the quality of care you desire

for patients. This is the best way to test your motives, and can quickly steer decisions back to a place of perspective.